Executive Summary

- Capital has migrated up the risk curve: A decade of inflows into direct lending has outpaced growth in the core middle market, pushing managers into large-cap unitranche deals and weaker credits. The headline yield premium over investment grade has narrowed even as the underlying risk profile of new originations has widened.

- Covenant erosion and PIK are accumulating unrealized risk: Covenant-lite structures and payment-in-kind toggles, once confined to the broadly syndicated loan market, now permeate significant portions of direct lending. Both remove the early-warning function of maintenance covenants and mask cash-flow deterioration, setting up sharper realized losses than historical middle-market recovery rates would imply.

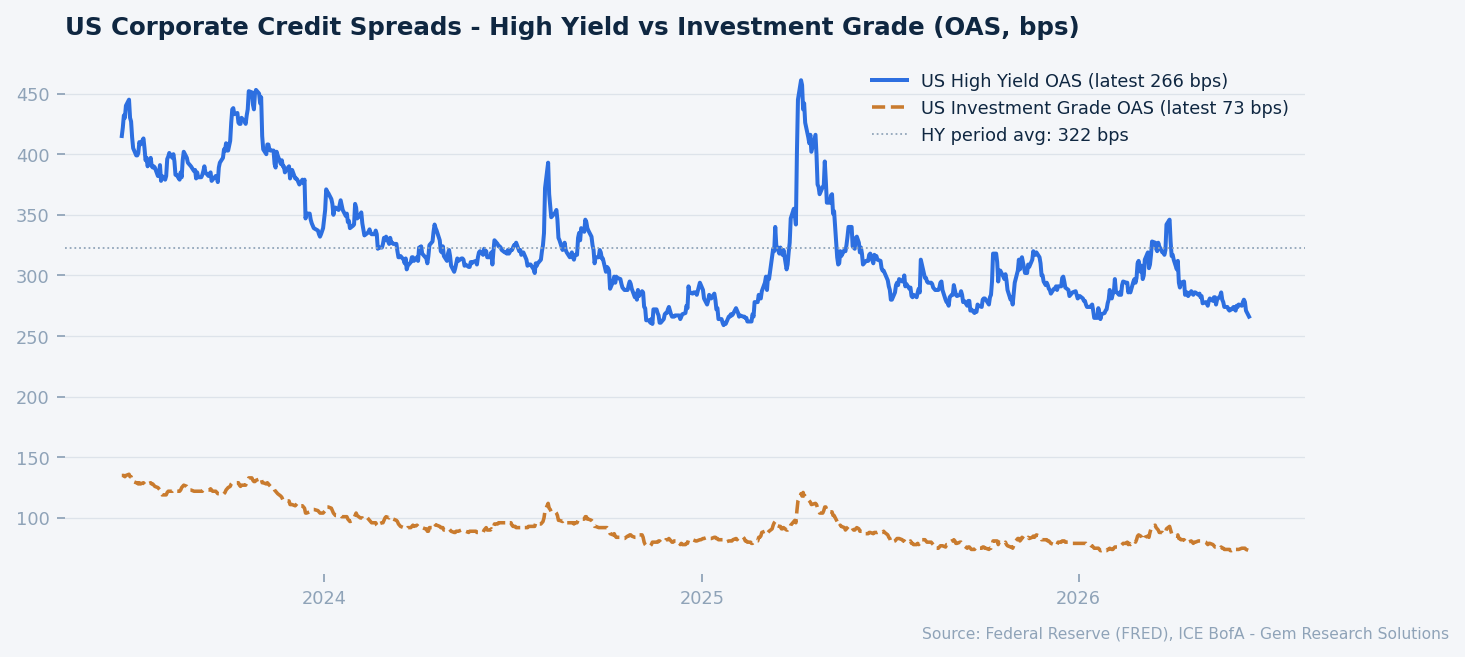

- Public credit markets offer almost no buffer: US high-yield spreads sit near 266 basis points against a period average of roughly 322, and investment-grade spreads near 73 versus an average of about 94 (Federal Reserve Economic Data). Tight spreads reflect strong risk appetite, not a margin of safety, and leave little room to absorb a repricing.

- A refinancing wall is approaching regardless of rate path: With the effective federal funds rate at 3.63% and the 10-year Treasury at 4.47%, floating-rate 2021 and 2022 vintage loans underwritten at thin coverage face a maturity cohort over the next 18 to 30 months. Whether it resolves through refinancing or amendment activity depends on whether the Fed continues easing or pauses against headline CPI still running near 4.2%.

Market Overview

The private credit market has spent the better part of a decade positioning itself as the institutional alternative to broadly syndicated loans and high yield bonds. That positioning worked. Assets under management in direct lending strategies expanded dramatically through the rate hiking cycle, partly because floating-rate structures benefited lenders as the Fed moved, and partly because banks constrained by capital requirements stepped back from leveraged lending. What has changed is not the demand for the asset class but where that capital is now being deployed, and on what terms.

The macro backdrop frames the analysis. The effective federal funds rate stands at 3.63% following a measured easing cycle, the 10-year Treasury yields 4.47%, and headline CPI held near 4.2% through May 2026, per Federal Reserve data. Equity markets remain elevated, with the S&P 500 above 7,500, and public credit spreads are compressed. This is a benign surface environment. The structural conditions building beneath it, however, point to a more demanding period ahead for credit underwritten during the boom.

From Middle Market to Broadly Leveraged Borrowers

The original pitch for direct lending was disciplined, relationship-based credit to the core middle market: companies with $10 million to $75 million in EBITDA, tight documentation, meaningful covenants, and lender-friendly structures. That segment still exists, but the capital chasing it has grown far faster than the addressable borrower pool. The result is predictable: yield compression in the core middle market drove managers up the risk curve.

The expansion has taken two directions. Direct lenders have moved into large-cap unitranche deals, competing with or replacing syndicated credit on transactions that would historically have tapped the broadly syndicated loan market. They have also extended into borrowers with weaker credit profiles, thinner EBITDA coverage, and in some cases more speculative business models. Both moves increase exposure to tail-risk outcomes while the headline yield premium over investment grade has narrowed.

Covenant Erosion and Recovery Risk

The covenant-lite structure that became standard in the broadly syndicated loan market after 2010 has now migrated into significant portions of the direct lending market. This matters because covenants serve a function beyond restricting borrower behavior: they are an early warning system. Maintenance covenants, when they exist, trigger technical defaults well before a borrower exhausts liquidity, giving lenders time to restructure before value has been impaired.

In a covenant-lite structure, that early warning is absent. Lenders are exposed to a borrower until it cannot service its debt or misses a payment. By that point in a deteriorating credit situation, recovery values are typically lower because the borrower’s enterprise value has already declined. The practical consequence is that in the next stress cycle, private credit portfolios with high concentrations of covenant-lite paper are likely to experience sharper realized losses than historical middle market recovery rates would suggest.

Compounding this is the spread of payment-in-kind, or PIK, interest structures. PIK toggles allow borrowers to defer cash interest payments by accruing additional principal. While these structures can preserve liquidity for a distressed borrower, they also mask deterioration in portfolio quality. A borrower opting into PIK is signaling cash flow strain. A portfolio with rising PIK concentrations is accumulating unrealized risk that will appear in reported marks only later in the cycle.

Reading the Current Market Signals

The current credit environment presents a mixed picture. US high yield spreads have compressed to approximately 266 basis points over comparable Treasuries, well inside the period average near 322 basis points, and investment grade spreads sit near 73 basis points against an average of roughly 94, both per Federal Reserve Economic Data. Tight public market spreads indicate benign credit sentiment, but they also reflect strong demand from investors reaching for yield in an environment where the 10-year Treasury yields 4.47%. The signal is not that credit is safe; it is that the market is paid very little to hold it.

US corporate credit spreads, high yield versus investment grade (OAS, bps). Both sit below their multi-year averages. Source: FRED, ICE BofA.

| Indicator | Current Level | What It Signals |

|---|---|---|

| US HY Credit OAS | ~266 bps | Compressed vs ~322 bps avg; risk appetite elevated |

| US IG Credit OAS | ~73 bps | Near cycle tights; thin spread buffer |

| 10Y Treasury Yield | 4.47% | Elevated cost of capital for refinancings |

| Fed Funds Rate (effective) | 3.63% | Floating-rate debt burden remains significant |

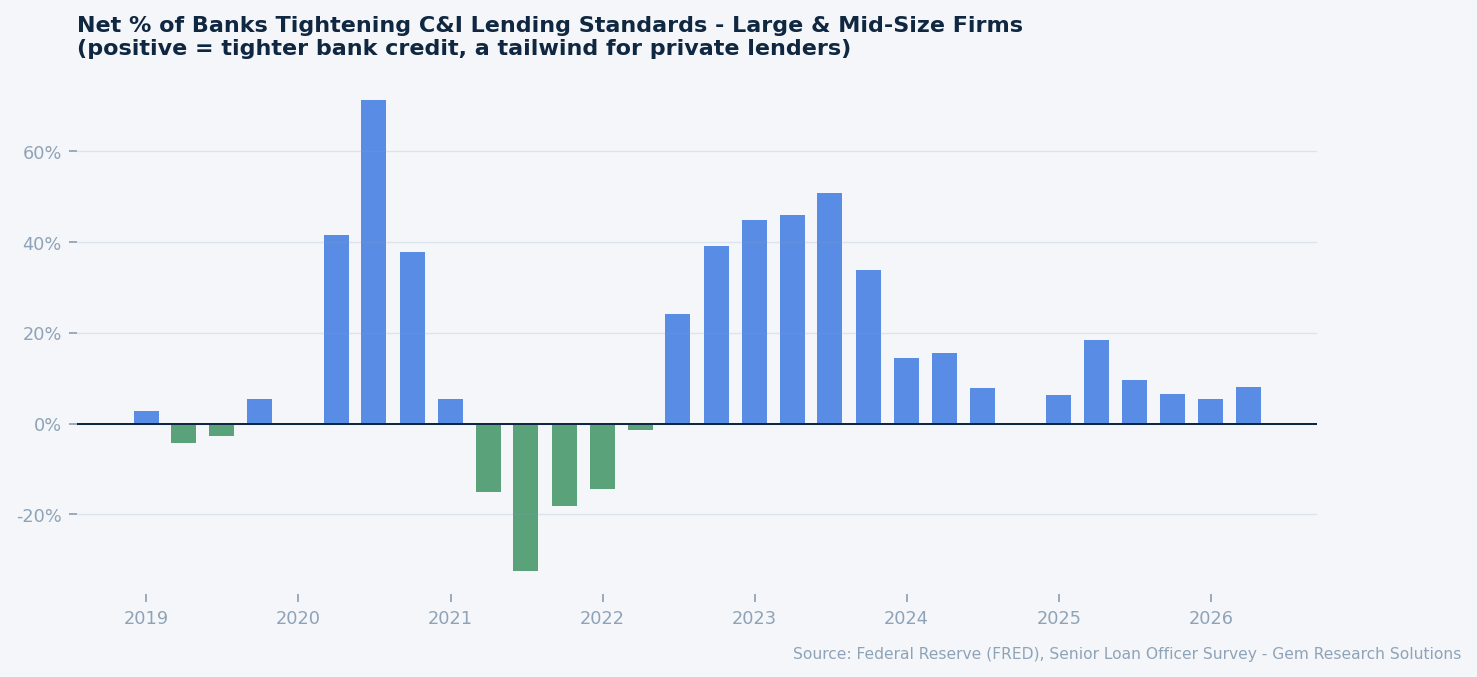

| Senior Loan Officer Survey (net % tightening, large/mid firms) | 8.1% | Bank standards tightening; borrowers migrating to private credit |

The Senior Loan Officer Opinion Survey data through April 2026 shows a net 8.1% of banks tightening standards for large and middle-market firms, per Federal Reserve data. When bank standards tighten, borrowers migrate toward private credit. This dynamic has historically supported direct lending volume, but it also means the marginal borrower entering private credit channels is one that banks have determined carries risk they are unwilling to hold on their own books.

Net % of banks tightening C&I lending standards, large and mid-size firms. Positive readings push borrowers toward private lenders. Source: FRED, Senior Loan Officer Opinion Survey.

The Refinancing Dimension

With the effective federal funds rate at 3.63%, floating-rate private credit loans originated in 2021 and 2022 under more aggressive underwriting assumptions are carrying coupons well above the entry-level projections that justified their initial valuations. For borrowers with sufficient cash flow, this is manageable. For those underwritten at thin coverage ratios who are now servicing debt at SOFR plus 600 or 700 basis points, the arithmetic is considerably more difficult.

The refinancing question becomes acute as large cohorts of 2021 and 2022 vintage private credit maturities approach over the next 18 to 30 months. In a benign scenario, rates continue declining and borrowers refinance at tighter spreads and lower base rates. In a scenario where inflation remains elevated, with headline CPI near 4.2% through May 2026 per Federal Reserve data, and the Fed pauses its cutting cycle, maturity extensions and amendment activity become the primary tool for managing distress without triggering formal restructuring processes.

Risk Factors

Covenant-lite recovery shortfall in the next stress cycle. The migration of covenant-lite and PIK structures into direct lending means the asset class will enter its first genuine downturn with weaker creditor protections than its track record was built on. Recovery rates that historically supported middle-market underwriting assumptions are unlikely to hold for portfolios concentrated in covenant-lite paper, and losses will surface later and more abruptly than reported marks currently imply.

Refinancing wall meeting a higher-for-longer rate path. The 2021 and 2022 origination cohorts were underwritten against an expectation of lower base rates by the time they matured. With the effective federal funds rate at 3.63% and headline CPI near 4.2%, a Fed pause would leave thinly covered borrowers refinancing into rates well above their original assumptions. The result is rising amendment-and-extend activity, deferred rather than resolved distress, and a lengthening tail of impaired credits carried at par.

Spread compression leaves no buffer. With high yield at 266 basis points and investment grade at 73, both well inside their multi-year averages per FRED, public credit is priced for a continuation of benign conditions. Private credit marks, which reference these public comparables, are similarly elevated. A normalization of spreads toward period averages would pressure NAVs across the asset class even without a rise in actual defaults.

Stress Signals Worth Tracking

For investors and analysts monitoring private credit portfolios, several leading indicators merit attention as the cycle progresses:

- BDC premium to NAV: Business development company shares trading at steep discounts to net asset value have historically preceded broader private credit stress, as public market investors price in NAV impairment well ahead of official marks.

- Amendment and waiver frequency: A rising rate of covenant amendments and waiver requests across direct lending portfolios indicates borrower distress that has not yet surfaced in reported non-accrual figures.

- NAV financing growth: Lenders extending credit against the net asset value of private credit funds rather than against underlying portfolio companies can obscure leverage concentration risk at the fund level and reduce transparency into true portfolio quality.

- PIK accrual rates: Disclosed PIK concentrations in BDC and private credit fund filings are among the cleaner early indicators of cash flow deterioration across a portfolio, appearing before non-accruals in most cases.

- Manager return dispersion: As the cycle matures, the spread between top quartile and bottom quartile manager performance typically widens. Narrowing return dispersion in a rising-risk environment can indicate that weaker managers are marking positions aggressively rather than reflecting genuine portfolio stability.

Gem Research Perspective

Gem Research’s analytical call on private credit is that the asset class is not in crisis, but it is past the point where growth and quality move together. Public credit spreads are tight, equity markets remain elevated with the S&P 500 above 7,500, and the default environment has been manageable. Beneath that surface, the structural conditions for a more difficult period are accumulating: covenant erosion, expansion into weaker credits, the floating-rate burden on 2021 and 2022 vintage borrowers, and a refinancing wall that will arrive over the medium term regardless of base rate direction.

The defining feature of this asset class is that it reprices slowly. Unlike a public bond market selloff, private credit deterioration surfaces through NAV markdowns, amendment activity, and non-accrual recognition that can lag underlying borrower stress by multiple quarters. By the time impairment appears in reported figures, the inflection will likely have occurred months earlier across the leading indicators described above. That lag is precisely why the watch list matters more than the headline default rate.

For allocators currently assessing private credit exposure, the relevant question is not whether the market has grown, but how that growth has been underwritten. We weight manager selection, covenant quality, and PIK concentration far more heavily than headline yield in the current environment, and we expect the dispersion between disciplined and undisciplined lenders to become the defining performance story of the next two years.