Executive Summary

- Global private credit AUM has crossed $3.5 trillion, with North American direct lending alone growing sevenfold since 2015, per AIMA and Preqin data — a scale that now rivals segments of the leveraged loan and high-yield bond markets combined.

- Bank retrenchment is structural, not cyclical: formalised originate-and-distribute partnerships between JPMorgan, Citigroup, Wells Fargo and counterparts including Apollo, Centerbridge, and Ares represent a durable credit-supply architecture that does not unwind with the rate cycle.

- Default stress is rising and cannot be dismissed as noise: Fitch Ratings reports US private credit default rates reached 6.0% in April 2026, a record high, with “bad PIK” (distressed payment-in-kind deferrals) at 6.4% of total private debt volume in Q1 2026 — concentrated in 2021-2022 vintage, covenant-lite loans.

- The structural-versus-cyclical verdict is not binary: the bank-partnership model is permanent; the current vintage stress is cyclical but non-trivial. Regulatory opacity — not solvency — is the primary near-term risk, as the FSB’s May 2026 vulnerability report and parallel SEC fraud investigations signal an oversight regime in formation.

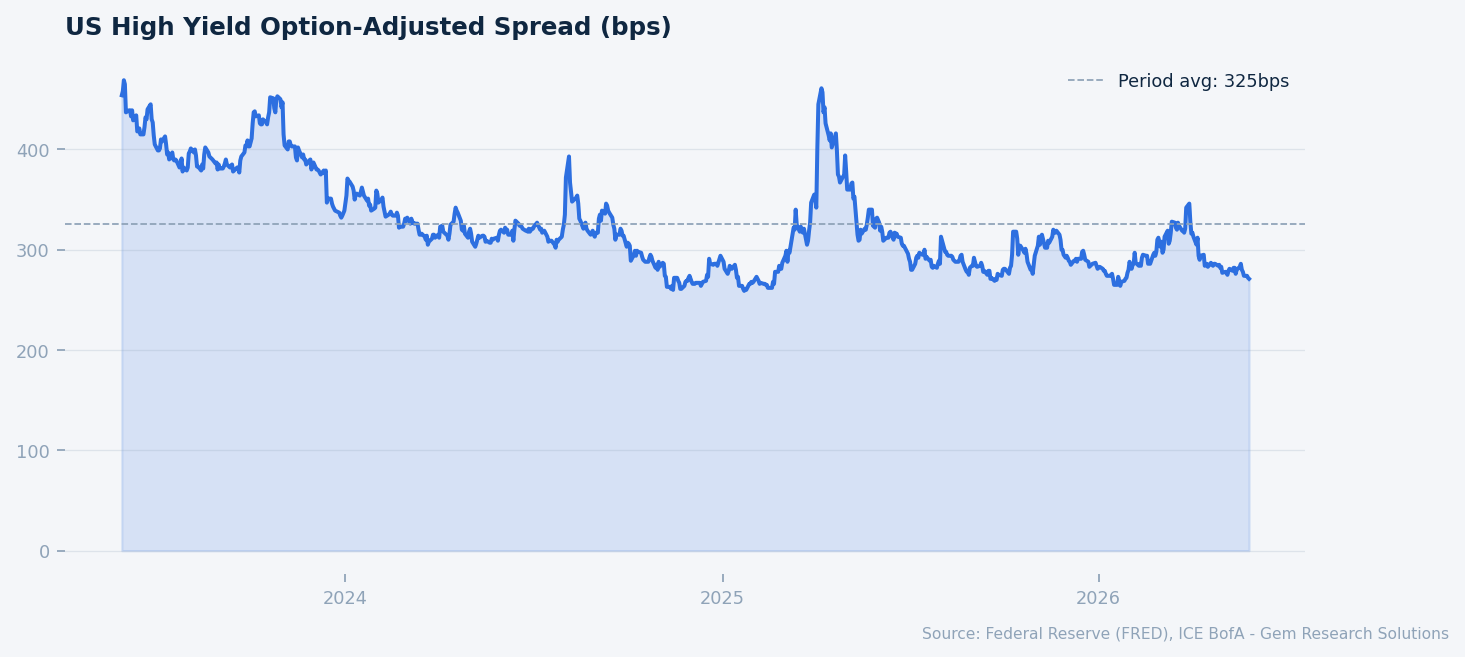

US High Yield OAS (bps). Source: FRED, ICE BofA.

Market Overview

Private credit — broadly defined as non-bank lending encompassing direct lending, mezzanine, distressed debt, and specialty finance — entered 2026 as one of the fastest-growing segments in global capital markets. Per AIMA, global AUM crossed $3.5 trillion during 2025, a figure that would have seemed implausible at the asset class’s emergence in the early 2000s. Preqin data place North American direct lending at approximately $644 billion by end-2025, up from $93 billion in 2015 — a sevenfold expansion in a single decade. Capital deployment accelerated sharply in 2024, reaching $592.8 billion, a 78% year-on-year increase, before continuing at pace: April 2026 alone saw $254 billion in disclosed private credit activity, with $167 billion attributable to fund closes, per Inforcapital.

To contextualise the market’s credit environment: as of May 2026, US High Yield Option-Adjusted Spreads stand at 271 basis points per Federal Reserve and ICE BofA data, materially inside the long-run period average of approximately 330 basis points. Investment-grade OAS sits at 74 basis points, likewise well inside its historical average of around 120 basis points. These are tight conditions. The compression in public credit spreads has functionally pushed yield-seeking institutional capital — pension funds, insurance companies, sovereign wealth funds, and family offices — toward private alternatives where illiquidity premiums remain intact. At the same time, the 10-year Treasury yield holds at 4.48% per Federal Reserve data, and the Fed Funds Rate sits at 3.64% following the 2022-2023 tightening cycle, meaning the floating-rate structures predominant in direct lending are simultaneously delivering attractive all-in yields and applying sustained debt-service pressure to mid-market borrowers.

The top five managers — Apollo, Ares, Blackstone, Carlyle, and KKR — collectively manage an estimated $1.5 trillion in perpetual capital, representing roughly 40% of their combined AUM. Blackstone’s BCRED vehicle alone stands at $83 billion. Mordor Intelligence projects the market to reach $3.48 trillion by 2031 at a 12.13% CAGR. The central analytical question is whether that trajectory reflects durable structural realignment of credit intermediation or a cyclically amplified surge that will partially retrace once rates normalise and bank lending standards ease.

Bank Retrenchment and the Great Credit Migration

The most consequential driver of private credit’s growth is not investor demand per se — it is the retrenchment of regulated banks from middle-market leveraged lending. This dynamic predates the 2022 rate cycle but was substantially accelerated by it. The Basel III Endgame regulatory proposals — first advanced by US regulators in 2023 — injected material uncertainty into bank capital planning even before their scope was revised and softened in subsequent iterations, per PwC’s Basel III Endgame tracker. Banks responded not by waiting for legislative clarity but by repositioning balance sheets proactively. Middle-market leveraged lending — transactions below approximately $500 million enterprise value — became the primary casualty. Direct lenders, unconstrained by risk-weighted asset calculations, stepped into that vacuum. Direct lending now finances roughly 90% of buyout transactions in the sub-$500 million EV category, per Preqin estimates.

The more architecturally significant development, however, is not pure displacement but formalised co-dependency. In February 2025, JPMorgan formalised a $50 billion direct lending commitment, syndicating origination risk to private credit partners. Citigroup announced a $25 billion partnership with Apollo. Wells Fargo established Overland Advisors in partnership with Centerbridge Partners, with an initial $5 billion commitment. These arrangements represent an originate-and-distribute model in which bank franchise value — relationship origination, distribution infrastructure, regulatory relationships — is preserved while duration and credit risk are transferred off balance sheet into BDCs and private credit funds. This model is structurally stable. It does not depend on rates remaining elevated, on bank capital rules remaining restrictive, or on any single macroeconomic scenario. It survives rate normalisation because the banks have already restructured their credit business models around it.

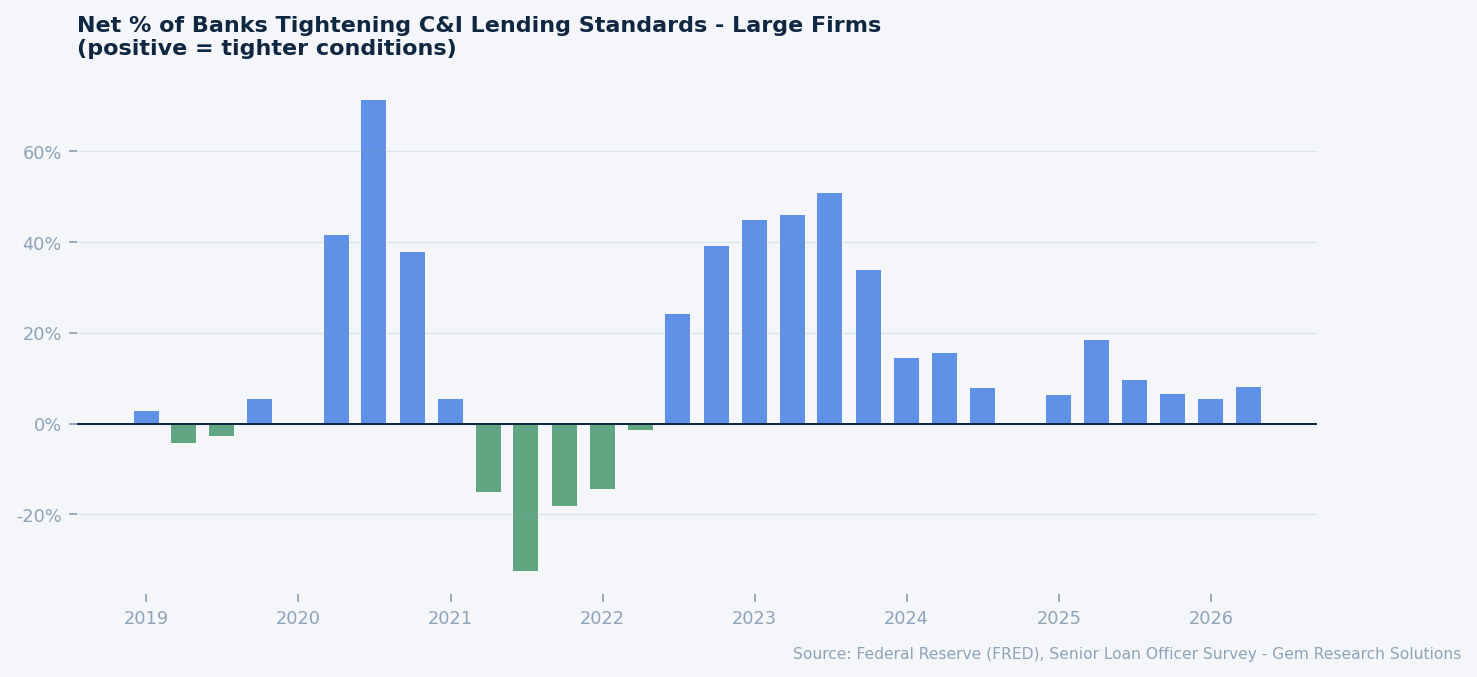

As of Q1 2026, the net percentage of banks tightening commercial and industrial lending standards, per the Federal Reserve Senior Loan Officer Opinion Survey, has eased from the extreme levels reached during the 2022-2023 tightening cycle but remains positive — meaning banks continue to tighten on net, albeit less aggressively. This sustained, if moderated, tightening continues to support direct lender origination volumes independent of the rate environment.

Net % of banks tightening C&I lending standards. Source: FRED, Senior Loan Officer Survey.

Mega-Fund Consolidation and the Perpetual Capital Advantage

Private credit’s structural shift is inseparable from the asset management industry’s pivot to perpetual capital structures. The BDC (Business Development Company) model, the BCRED format pioneered by Blackstone, and analogous continuously offered funds allow the largest managers to deploy capital at scale without the vintage-year concentration risk that characterises closed-end drawdown funds. Blackstone’s BCRED at $83 billion is the most prominent example, but Apollo, Ares, KKR, and Blue Owl each operate comparable vehicles. The aggregate perpetual capital pool managed by the top five firms — approximately $1.5 trillion — insulates these platforms from the liquidity dynamics that would otherwise constrain more traditional fund structures.

The pace of capital formation in early 2026 reinforces this point. The $254 billion in private credit activity recorded in April 2026 alone, per Inforcapital, is not a rounding error — it reflects the institutionalisation of the asset class. Insurance company allocations are particularly notable: liability-driven investors with long-duration obligations have matched private credit’s floating-rate, illiquid profile against annuity books and pension liabilities, creating structurally sticky demand. Apollo’s Athene platform is the most-cited example of this integration, but the dynamic is industry-wide.

Concentration, however, cuts both ways. The top-five manager dominance means that stress at a single platform — whether from valuation disputes, redemption pressure in a semi-liquid vehicle, or regulatory action — has system-wide implications. Fortune’s March 2026 reporting described a $265 billion market stress event simultaneously affecting Blackstone, KKR, Apollo, and Ares, driven by legacy vintage performance issues. The incident did not trigger systemic contagion, but it illustrated the degree to which the private credit ecosystem is now co-correlated at the top. Diversification across managers does not deliver the same risk reduction it once did when the asset class was genuinely fragmented.

Default Cycles, Vintage Risk, and the PIK Inflection

The bullish structural narrative must be assessed alongside a deteriorating credit performance picture that is not adequately captured by public market indicators. Fitch Ratings reported US private credit default rates reached 6.0% in April 2026, a record high, up from 5.8% in January and materially above the asset class’s historical average. “Bad PIK” — distressed payment-in-kind deferrals, as opposed to PIK elected from a position of borrower strength — reached 6.4% of total private debt volume in Q1 2026. These figures are not uniformly distributed: consumer discretionary sector exposures have been hit hardest, reflecting the specific underwriting environment of 2021-2022 vintages.

The 2021-2022 period was characterised by peak competition among direct lenders, near-zero base rates, and a sponsor-friendly underwriting environment that produced covenant-lite structures, elevated leverage multiples, and compressed documentation protections. Those loans are now maturing or approaching maturity in an environment where the effective all-in cost of capital is 400-500 basis points higher than at origination. Borrowers that cannot refinance face a binary outcome: amend-and-extend (which typically manifests as PIK election or maturity extension) or default. The 6.4% bad PIK rate suggests the amend-and-extend route is being heavily utilised, deferring but not eliminating credit losses and compressing realised returns below modelled expectations for affected vintages.

The valuation question is the central analytical risk. Private credit portfolios are marked to model, not to market. Unlike publicly traded high-yield bonds — where the 271 basis point OAS provides a real-time market clearing signal — private credit NAVs are updated quarterly by managers using internal models. If bad PIK and default rates continue to rise through mid-2026, the gap between model-implied valuations and economic reality will attract both regulatory scrutiny and investor attention. JPMorgan CEO Jamie Dimon has publicly flagged the valuation transparency issue. The FSB’s May 2026 vulnerability report formalised this concern at a multilateral regulatory level.

Risk Factors

Regulatory overhang and transparency risk. The Financial Stability Board’s formal “Report on Vulnerabilities in Private Credit,” published May 6, 2026, represents the most authoritative multilateral statement to date on the asset class’s systemic implications. In the United States, the Federal Reserve has issued information requests to major banks regarding private credit exposure. The SEC and CFTC jointly proposed Form PF amendments in April 2026 targeting enhanced data collection on loan maturity profiles, liquidity, and credit quality. SEC Chair Atkins simultaneously characterised private credit as non-systemically risky while confirming active fraud investigations — a posture that signals regulatory uncertainty rather than clarity. The risk is not immediate regulatory action but the chilling effect of an unclear and evolving oversight framework on capital formation and secondary market liquidity.

Rate persistence and floating-rate debt-service stress. With the Fed Funds Rate at 3.64% and core PCE inflation at 2.99% per BLS data — above the Federal Reserve’s 2% target — the rate environment does not support the aggressive easing scenario that would materially ease floating-rate debt-service burdens. If rates remain above 3.5% through 2026 and into 2027, the 2021-2022 vintage stress cycle will extend, pushing default rates potentially above 7% and forcing wider recognition of portfolio impairment. The 10-year Treasury at 4.48% and a broad dollar index at 119.3 per Federal Reserve data indicate that global rate and currency dynamics do not provide a relief valve.

Concentration and co-correlation at the platform level. The consolidation of private credit into five dominant managers, each running perpetual capital vehicles with retail distribution (BDCs, interval funds), creates a structural vulnerability that did not exist when the asset class was smaller and more fragmented. A redemption event at a major semi-liquid vehicle — triggered by performance concerns, a liquidity event, or a regulatory action — could force asset sales into an illiquid market at a moment when other platforms face identical pressure.

Gem Research Perspective

Our analytical call is unambiguous on the structural question and more cautious on the cyclical one. Bank retrenchment from middle-market lending is permanent. The originate-and-distribute partnerships formalised in 2024-2025 by JPMorgan, Citigroup, and Wells Fargo represent a restructuring of credit intermediation infrastructure that will not reverse in the next rate cycle or the one after it. On this dimension, private credit’s growth trajectory is structural.

The cyclical dimension, however, presents a real and underappreciated risk window spanning approximately 12 to 24 months from the date of this report. The 2021-2022 vintage maturity wall, combined with sustained elevated rates and rising bad PIK volumes, creates conditions in which reported NAVs at several mid-tier and large managers could face downward revision. We do not anticipate systemic contagion — the perpetual capital structures of the top-five platforms insulate them from classic run dynamics. But we do expect a meaningful valuation correction event in one or more high-profile vehicles before end-2026, which will accelerate regulatory action and compress retail allocations into the asset class temporarily.

Investors and analysts should watch three variables closely: the trajectory of Fitch’s private credit default rate through Q3 2026 (a sustained move above 7% would be the signal); the substance of final Form PF amendments when promulgated; and the pace of Fed rate cuts — each 25-basis-point reduction materially eases debt-service pressure on the most stressed 2021-2022 vintage borrowers. The asset class is here to stay. The next 18 months will determine who manages it credibly and who does not.